Contents

Overview

The concept of financial entities predates modern corporations, tracing back to ancient systems of record-keeping for trade and taxation. Early forms included merchant partnerships in Mesopotamia and the Roman Empire, which managed shared ventures and profits. The development of double-entry bookkeeping in 14th-century Italy, notably by Luca Pacioli, provided a standardized method for tracking financial transactions, laying the groundwork for more sophisticated entities. The rise of joint-stock companies in the 17th century, such as the Dutch East India Company (founded 1602), allowed for pooled capital and limited liability, transforming business structures and enabling large-scale ventures like colonial expansion and global trade. This era saw the formalization of entities designed for profit, investment, and governance, setting the stage for the diverse financial landscape we see today.

⚙️ How They Function

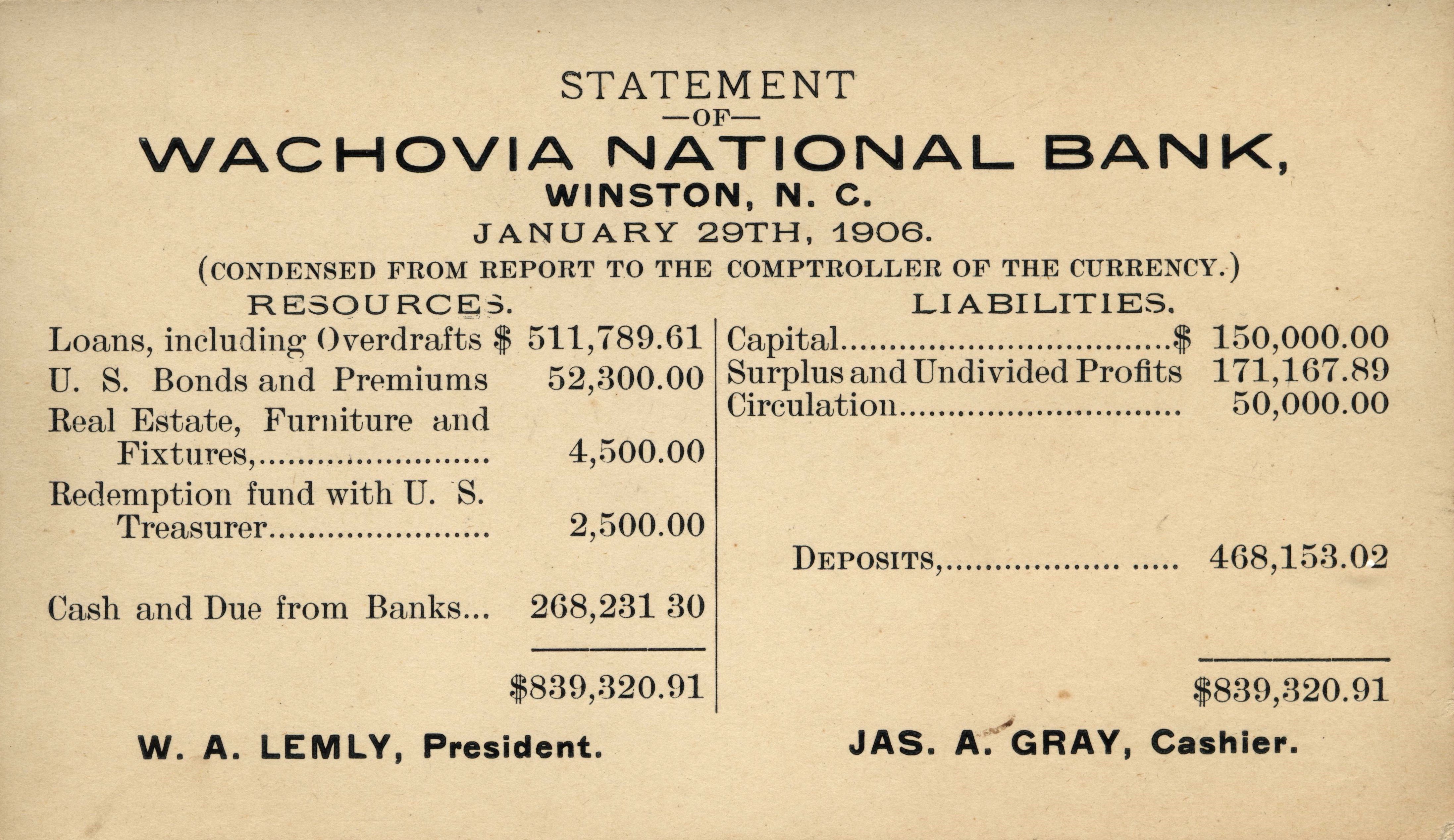

At their core, financial entities operate by managing flows of money and value. They can be broadly categorized into individuals (managing personal finances), businesses (seeking profit or providing services), non-profits (pursuing social missions), and governments (managing public funds and policy). Each entity maintains financial records, including balance sheets detailing assets and liabilities, income statements showing profitability over time, and cash flow statements tracking liquidity. These records are essential for internal management, external reporting to stakeholders like investors and creditors, and compliance with regulatory bodies such as the SEC in the United States or the European Central Bank in the Eurozone. The complexity of their operations often necessitates specialized software and professional expertise in accounting and finance.

📊 Key Facts & Numbers

The global financial system comprises an astonishing number of entities. There are over 1.7 billion bank accounts worldwide, managed by thousands of financial institutions. The total value of assets under management by global investment firms exceeded $100 trillion in 2023, a figure that has grown exponentially since the turn of the millennium. Publicly traded companies number in the tens of thousands on major exchanges like the NYSE and Nasdaq, with market capitalizations often reaching hundreds of billions or even trillions of dollars, like Apple Inc. or Microsoft. The sheer volume of transactions processed daily by these entities, estimated in the quadrillions of dollars across all markets, underscores their immense scale and interconnectedness.

👥 Key Players & Structures

Financial entities manifest in various forms, each with distinct governance and operational models. Individuals manage their finances through personal accounts, while small businesses might operate as sole proprietorships or partnerships. Larger entities include corporations, which can be privately held or publicly traded on stock exchanges, offering shares to investors. Investment vehicles like mutual funds, hedge funds, and private equity firms pool capital from multiple investors to deploy in various assets. Non-profit organizations, such as the Red Cross or Doctors Without Borders, manage funds for charitable purposes, while governments and their agencies, like the Federal Reserve, oversee monetary policy and public finance. Key figures within these entities include CEOs, CFOs, fund managers, accountants, and regulators.

🌍 Global Reach & Impact

The influence of financial entities extends across every corner of the globe, shaping economies and societies. Multinational corporations like JPMorgan Chase and HSBC operate in numerous countries, facilitating international trade and investment. Sovereign wealth funds, such as Norway's Government Pension Fund Global, manage vast national assets, impacting global markets. The flow of capital through these entities dictates investment patterns, job creation, and economic development, often with significant geopolitical implications. Regulatory bodies worldwide collaborate, albeit imperfectly, to manage systemic risks and ensure a degree of stability, as seen in the coordinated responses during the 2008 financial crisis.

⚡ Current Trends & Innovations

The financial entity landscape is constantly being reshaped by technological innovation. Fintech startups are challenging traditional institutions with new platforms for payments, lending, and investment, such as PayPal and Robinhood. The adoption of AI and machine learning is revolutionizing risk assessment, fraud detection, and algorithmic trading. Blockchain technology and cryptocurrencies are exploring decentralized models for asset management and transaction processing, potentially altering the role of intermediaries. Open banking initiatives are also fostering greater data sharing and competition among financial entities.

🤔 Controversies & Criticisms

Despite their essential role, financial entities are frequently embroiled in controversy. Issues of transparency and accountability are perennial concerns, particularly with complex derivatives and off-balance-sheet vehicles that can obscure risk, as highlighted during the Enron scandal. The concentration of power within a few large institutions raises questions about market manipulation and systemic risk, leading to calls for stricter regulation and antitrust actions. Ethical debates surround executive compensation, the impact of high-frequency trading, and the role of financial institutions in funding environmentally damaging industries. The pursuit of profit can sometimes conflict with broader societal well-being, creating ongoing tension.

🔮 Future Trajectories

The future of financial entities points towards increased digitalization, decentralization, and personalization. We can expect further integration of AI and machine learning to drive hyper-personalized financial advice and automated portfolio management. The rise of DeFi could significantly disrupt traditional banking and investment models, offering alternatives to centralized intermediaries. Regulatory frameworks will continue to adapt, grappling with the challenges posed by new technologies and globalized markets. The ongoing debate will likely focus on balancing innovation with stability, ensuring that financial entities serve the broader economy rather than solely their own interests. The potential for new forms of digital assets and ownership structures also looms large.

💡 Practical Applications

Financial entities are fundamental to nearly every aspect of modern life. Individuals use them daily for managing salaries, paying bills, saving for retirement, and obtaining mortgages through entities like Bank of America. Businesses rely on them for funding operations, managing payroll, and facilitating sales via payment processors like Stripe. Governments use them to collect taxes, issue debt, and manage national budgets. Investment entities provide capital for startups and established companies, driving innovation and economic growth. Even non-profits depend on financial entities to manage donations and fund their missions, demonstrating their pervasive reach.

Key Facts

- Year

- Ancient origins, continuously evolving

- Origin

- Global

- Category

- technology

- Type

- concept

Frequently Asked Questions

What are the main types of financial entities?

Financial entities can be broadly categorized into individuals managing personal finances, businesses (corporations, partnerships, sole proprietorships) focused on profit, non-profit organizations pursuing social missions, and governmental bodies managing public funds. Within these, specialized entities like banks, investment funds (mutual funds, hedge funds), insurance companies, and regulatory agencies play critical roles in the financial ecosystem. Each type has unique structures, objectives, and reporting requirements, contributing to the overall complexity and functionality of the global economy.

How do financial entities report their performance?

Financial entities report their performance through formal financial statements. The primary statements include the balance sheet, which provides a snapshot of assets, liabilities, and equity at a specific point in time; the income statement (or profit and loss statement), detailing revenues, expenses, and net income over a period; and the cash flow statement, tracking the movement of cash in and out of the entity from operating, investing, and financing activities. These statements are crucial for stakeholders like investors, creditors, and regulators to assess an entity's financial health, profitability, and liquidity.

What is the role of technology in financial entities?

Technology is fundamentally reshaping financial entities. Fintech innovations have introduced new platforms for payments, lending, and trading, increasing efficiency and accessibility. Artificial intelligence and machine learning are being deployed for advanced analytics, risk management, fraud detection, and personalized customer service. Blockchain technology is exploring decentralized finance (DeFi) models that could reduce reliance on traditional intermediaries. These technological advancements are driving competition, creating new business models, and demanding continuous adaptation from established financial institutions.

Why are financial entities so heavily regulated?

Financial entities are heavily regulated due to their critical role in the economy and the potential for systemic risk. Their activities involve managing vast sums of money, and failures can have cascading effects, as seen in the 2008 financial crisis. Regulations aim to ensure stability, protect consumers and investors from fraud and mismanagement, prevent money laundering, and maintain fair competition. Bodies like the SEC and central banks establish rules for capital requirements, transparency, and operational conduct to safeguard the financial system and public trust.

What are the main controversies surrounding financial entities?

Major controversies include issues of transparency, particularly with complex financial products that can obscure risk. The concentration of power among a few large institutions raises concerns about market manipulation and systemic risk, leading to debates about antitrust measures. Ethical dilemmas arise concerning executive compensation, the impact of high-frequency trading, and the financing of environmentally or socially harmful activities. The pursuit of profit can sometimes lead to practices that conflict with broader societal well-being, creating ongoing tension between financial interests and public good.

How do financial entities impact everyday life?

Financial entities are integral to daily life. Individuals use them for managing salaries, paying bills, saving for goals like retirement or homeownership through banks and investment firms. Businesses rely on them for loans, payment processing, and capital investment to operate and grow. Governments use financial entities to collect taxes and fund public services. The availability of credit, the stability of savings, and the efficiency of transactions all depend on the functioning of these entities, directly affecting personal financial security and economic opportunity.

What is the future outlook for financial entities?

The future points towards increased digitalization and decentralization. Expect greater integration of AI for personalized services and advanced analytics. Decentralized Finance (DeFi) built on blockchain technology could challenge traditional intermediaries, offering new models for lending, trading, and asset management. Regulatory bodies will continue to evolve their frameworks to address these innovations, seeking to balance growth with stability. The ongoing challenge will be to harness technology for broader economic benefit while mitigating risks and ensuring equitable access.